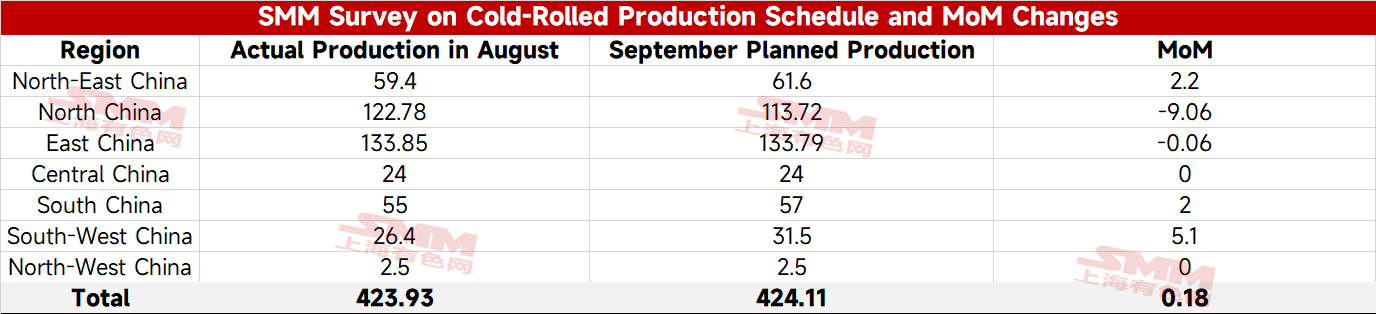

- SMM Cold Rolling Production Schedule: Steel Mills' Cold Rolling Output Fluctuates Rangebound in September

According to the latest SMM tracking data, 31 mainstream steel mills plan to produce a total of 4.2411 million mt of cold-rolled commodity coil in September, up 1,800 mt (0.04%) from the actual output in August. In terms of daily average, with one fewer day in September compared to August, the planned daily production stands at 141,400 mt, a 0.04% increase MoM from August's actual daily output.

- SMM HRC Production Schedule: September Daily Average HRC Output Up 0.5% MoM

According to the latest SMM tracking data, 39 mainstream steel mills planned a total HRC commercial material output of 14.0407 million mt in September, down 390,400 mt (2.7%) from the actual HRC commercial material production in August. On a daily average basis, with one fewer day in September compared to August, the planned daily HRC commercial material output for September stood at 468,000 mt, up 0.5% MoM from the actual daily HRC production in August.

In September, according to the SMM survey, steel mills in multiple regions including northeast China, north China, east China, central-south China, and western China announced annual maintenance or voluntary production cuts. Additionally, steel mill profits in September declined MoM from August, coupled with relatively moderate order-taking performance at some mills, which dampened their production expansion enthusiasm. Under these combined effects, the total hot-rolled production schedule of steel mills in September dropped by 390,400 mt MoM. As September has fewer days than August, the daily average hot-rolled production schedule remained basically stable MoM.

By trade type:

Domestic trade: The HRC domestic production schedule for September reached 13.1057 million mt, down 401,400 mt (3.0%) MoM from August's actual output. In daily average terms, with one fewer day in September than August, the surveyed steel mills' average daily HRC domestic schedule stood at 436,900 mt, up 0.3% MoM from August's actual daily commodity HRC production.

Export trade: September's HRC export schedule totaled 935,000 mt, up 11,000 mt (1.2%) MoM from the prior month's actual exports. Domestic mills' HRC export plans edged up slightly MoM. According to the SMM survey, some mills reported improved export order-taking due to the earlier intensified MD export investigations, preventing this month's export schedule from declining more than expected.

Summary:

In September, steel mills' daily average HRC production schedule increased slightly by 0.5% MoM compared to the actual output of the previous month, with relatively small fluctuations in daily levels.

Looking ahead, in terms of supply, HRC production schedules at steel mills remained basically stable MoM in September. Demand side, as September progresses, the transition between off-peak and peak seasons is gradually accelerating, leaving room for improvement in steel demand. HRC inventory is also expected to reach a destocking inflection point, with the supply-demand imbalance exerting relatively small downward pressure on prices.

Other factors: From a macro perspective, the US Fed's interest rate cut is anticipated in September, though the market may have already priced it in. Cost side, hot metal rebounded rapidly after production restrictions ended in early September, and steel mills began pre-holiday restocking in mid-to-late month, providing solid cost support. Under these combined influences, HRC prices are likely to edge up slightly in September, but the upside remains limited as the price ceiling window has yet to open.

![Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].](https://imgqn.smm.cn/usercenter/zUFfM20251217171748.jpg)

![[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)